Although the climate crisis started to become widely declared in the early 2000s, carbon-capture technology has been around in the US since the early 1970s as a tool for enhanced oil recovery. CCUS has long since been established in the energy sector as a crucial step towards mitigating the environmental damage from industrial activity following a global boom in net-zero strategies, climate goals and energy transition mania.

As with most technological breakthroughs, the US remains one of the bigger players in the carbon market. Global Energy Infrastructure (GEI) confirms an installed capacity to capture more than 28mt/yr in the US. Accounting for almost half of the global capacity, it stands as a world leader in carbon management. The question of the hour remains: with shifting US priorities and backsliding by higher-income nations contrasted by the expansion of carbon management in emerging markets, where does US carbon stand today?

As the century’s first quarter closes

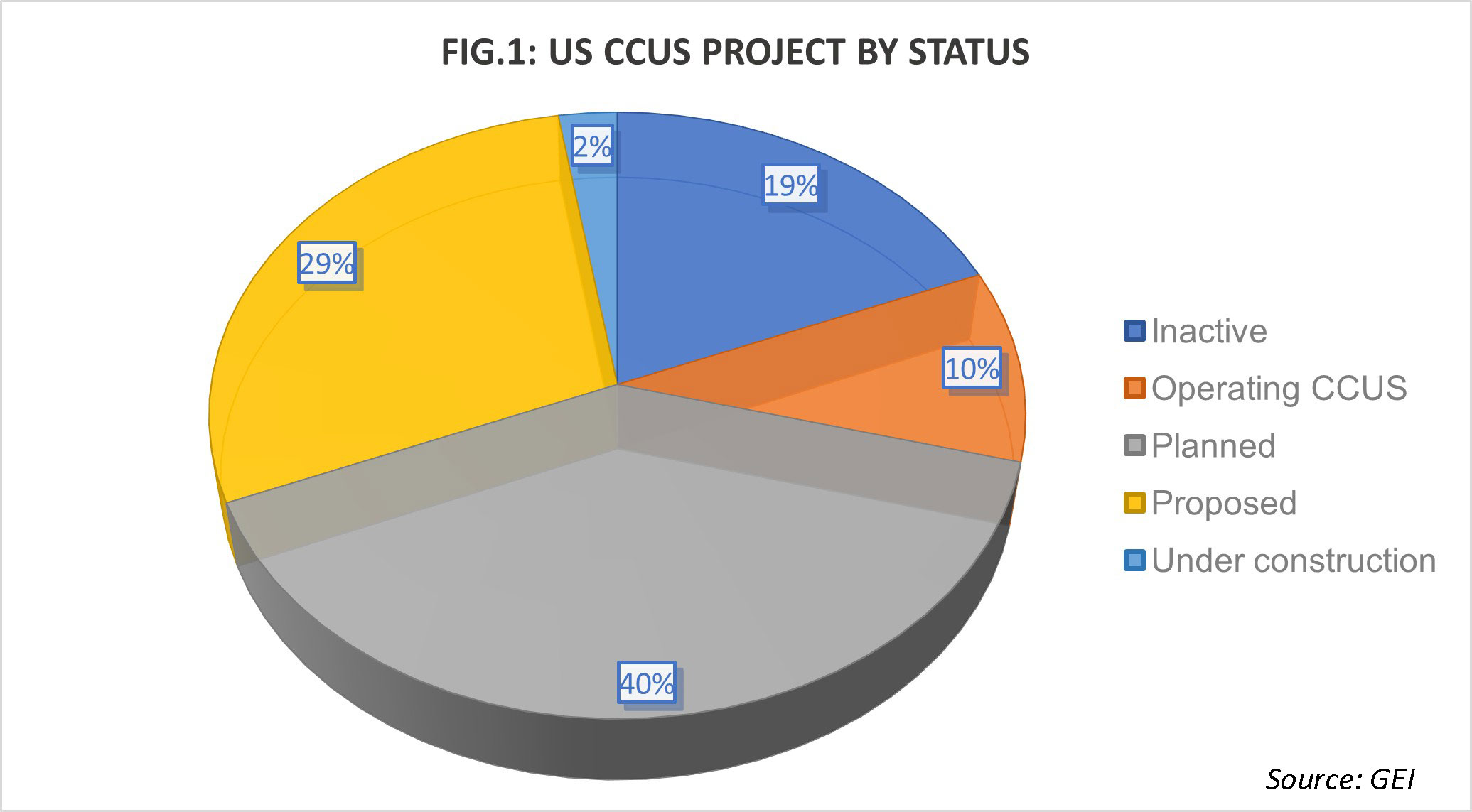

Our data at GEI reflects an intriguing dichotomy in the US CCUS market, with remarkable progress contrasting with institutional uncertainty. The market is characterised by a mix of operational and under-construction projects and significant scale-ups in planned capacity alongside a string of delays and cancellations. Project distribution shown in Fig.1 underscores the gap between announced ambitions and realised deployment.

Several CCUS projects have been axed due to permitting bottlenecks and political opposition, most notably in the state of Iowa along with some in South Dakota, Illinois and Nebraska. This is reflective of shifting tides in the national climate policy landscape since the start of the second Trump administration. By mid‑2025, the Department of Energy (DOE) cancelled $3.7b in previously awarded decarbonisation grants, including CCS demos, and moved to curtail or restructure clean‑energy offices—reducing certainty for grant‑dependent projects and pushing developers towards private finance and tax credit monetisation. At the same time, Congress enacted the One Big Beautiful Bill Act (OBBBA) on 4 July 2025, preserving and adjusting Section 45Q rather than repealing it, which has been a good change in certain cases.

To permit or not to permit?

The other decisive variable in GEI data is permitting. Multiple projects awaited Class VI approvals while Midwest pipeline corridors faced route changes and Public Utilities Commission denials, notably Summit Carbon Solutions in South Dakota in April 2025—pushing several ethanol plant schedules to 2026 or beyond. Conversely, primacy expansions are expected to accelerate saline storage approvals along the Gulf Coast, ultimately allowing better coordination and improved efficiencies for CCS projects.

Class VI wells remain a crucial infrastructure. As of September 2025, data from the US Environmental Protection Agency’s (EPA’s) UIC Class VI Permit Tracker shows Texas as the state with most pending Class VI well applications (26.8%), followed by California (23%), Alabama (20.1%) and other states (cumulatively, 30.1%).

The EPA has now approved the state of Texas’ request to administer permitting for Class VI underground injection wells on 12 November 2025. Texas will be able to implement Underground Injection Control (UIC) programmes covering all well-types (Class I-VI). Texas is now the sixth state to be granted Class VI well primacy after North Dakota in 2018, Wyoming in 2020, Louisiana in December 2023, West Virginia in February 2025 and Arizona in September 2025.

First movers and next steps

Last year saw the US CCS landscape defined by clustering around legacy basins and the Gulf Coast. Operational projects continue to be concentrated in states with early CO₂ infrastructure. Wyoming and North Dakota anchor legacy capture at LaBarge and Great Plains Synfuels, while ethanol-linked bioenergy with CCS (BECCS) sites cluster in the Upper Midwest. Fig.2 shows the distribution of installed capture capacity across operating CCUS projects, reinforcing the Lone Star State’s pioneering position in leading the charge on carbon capture.

FIG.2: INSTALLED CAPTURE CAPACITY IN THE US

| 500,000 | ||

| Kansas | ||

| Louisiana | 2,300,000 | |

| 500,000 | ||

When it comes to planned scale-up, the setup is overwhelmingly Gulf Coast-centric: Texas and Louisiana dominate future capacity with multimillion‑ton hubs tied to hydrogen, LNG and ammonia production, leveraging existing pipeline networks and deep saline formations. Projects such as Air Products’ Louisiana Clean Energy Complex, ExxonMobil’s Gulf Coast storage portfolio and Bayou Bend CCS illustrate how primacy approvals and industrial density create a cluster effect, reducing transport costs and enabling shared infrastructure. California forms a secondary cluster with Carbon TerraVault and Elk Hills CalCapture, leveraging depleted reservoirs for storage.

This geographic concentration reflects a strategic pivot; developers favour regions with geology, permitting authority and industrial emitters co-located to achieve economies of scale. Fig.3 provides a full picture of CCUS projects by state and status.

From plans to permits, and permits to injections

The US CCS market is ideally positioned for a significant scale-up. GEI analysis highlights a strong pipeline of under-construction and FID projects—such as Air Products’ Louisiana Clean Energy Complex (more than 5mt/yr), Nucor-ExxonMobil steel CCS (approximately 0.8mt/yr) and multiple Gulf Coast hubs scheduled—to start operations between 2026 and 2030. California’s Carbon TerraVault I and CalCapture will provide critical proof points for depleted-reservoir storage, while ethanol-linked BECCCS projects in the Midwest aim to regain momentum provided pipeline permitting hurdles are cleared. To that point, with Texas and Louisiana now holding Class VI primacy, permitting timelines for saline storage should compress and enable Gulf Coast clusters to leverage shared infrastructure and achieve economies of scale.

This year might mark the inflection from demonstration to deployment—if regulatory clarity and community engagement keep pace. GEI caveats this with the fact that some states are not prioritising permitting speed despite having funding and support—for example, a string of Navigator and POET projects have been cancelled across Iowa, Illinois and Nebraska due to local pushback.

Specifics to watch out for

As move into the new year, below are some of the key points to watch for the US carbon market in 2026 and beyond:

- The California storage template: Carbon TerraVault I and CalCapture as benchmarks for depleted-reservoir sequestration and California Environmental Quality Act -aligned permitting.

- Midwest ethanol integration: Summit Carbon Solutions’ pipeline reroute and permitting outcomes, which will be critical for unlocking more than 50 plant tie-ins

- Direct air capture (DAC) milestones: STRATOS (Oxy/1PointFive) will see its first operational year as wet commissioning is currently underway, with milestones to follow as more DAC projects receive Class VI permits

- Gulf Coast scale-up: Majority of planned or proposed CCUS projects are concentrated around Texas and Louisiana as primacy, geological and legacy advantages enable fast and efficient growth.

45Q continues to fuel growth for 2026

Under the Biden-era Inflation Reduction Act, the 45Q tax creidt offered $85/t for secure geologic storage and $180/t for DAC, with direct pay options and generous multipliers for projects meeting labour standards. These high-value credits, combined with DOE grants, fuelled a wave of hub announcements and early-stage engineering.

The OBBBA changed the landscape in 2025. DOE grants were largely eliminated, but 45Q was restructured rather than repealed. Baseline credit values now stand at $50/t for geologic storage and $36/t for DAC, with wage and apprenticeship multipliers retained, allowing effective rates to exceed $130/t for DAC and $85/t for point-source capture.

Additionally, EOR-linked credit has risen in line with CCS, making enhanced oil recovery more attractive for operators and reinforcing the Gulf Coast’s cluster strategy. The 12-year credit term and transferability provisions remain intact, ensuring developers can monetise credits without federal grants.

45Q’s durability implies that CCS remains commercially viable despite the absence of the previous grant-driven model, especially for large emitters and integrated players such as ExxonMobil.

Closing notes

As 2026 approaches, the US CCS market stands at a critical juncture. Clusters are forming, primacy is accelerating and tax incentives, though recalibrated, still remain robust. The next 12 months have the power to determine whether these building blocks translate into multi-megaton injections and durable climate impact, or stall under permitting and trust challenges.

Economic and policy dynamics will shape the pace of this scale-up. The Trump administration’s rollback of DOE grants and hub funding has shifted CCS economics toward tax-driven incentives under the revised 45Q credit, making private capital and credit transferability essential for project bankability.

With more than 90 projects planned, the US CCS pipeline signals ambition. But ambition alone will not cut emissions. Successful scale-up will hinge on collaboration between regulators, industry and communities. Aligning financing, transparency and infrastructure through stable 45Q monetisation; primacy-enabled permitting speed; and durable community engagement will ultimately push the US carbon market to deliver on climate goals.

While 2025 has cracked open the window for decisive action, 2026 promises a chance to seize it and define the decade.

Amulya James is a research analyst at Global Energy Infrastructure. This article is taken from our Outlook 2026 report. To read Outlook 2026 in full, click here.

Comments