The international steam coal market had an exceptional year in 2022, with prices touching record highs. In fact, the rally started in Q4 2020 due to the strong recovery from the Covid pandemic. The average of the main high calorific value (6,000kcal/kg NAR) international contracts (Fob Newcastle, Fob Richards Bay, Fob Colombia, Fob Indonesia and Fob Russia) assessed by Perret Associates bottomed out at $50.20/t in August 2020 and finished at $75.75/t in December.

To a large extent, 2021 was one-way traffic, with the same average prices rising to $232/t in October 2021 before dropping back to $151.30/t in December—still a very high level compared with the historical average at $70–75/t (at that time) since 2000.

Record high

The market started 2022 on a bearish footing, but a succession of supply constraints in Russia in January, due to very cold weather and a lack of railways cars, and Moscow’s invasion of Ukraine in February pushed the average of steam coal contracts to a historical high of $366/t on 11 March.

Most contracts—except for Russian material, which has since been sold at a significant discount—traded in an elevated trading range of $250–400/t until September 2022.

Most market participants expected the rally to resume, or at least for prices to remain flat in Q4 2022, as the full impact of the EU’s ban on Russian coal imports had taken full effect on 10 August.

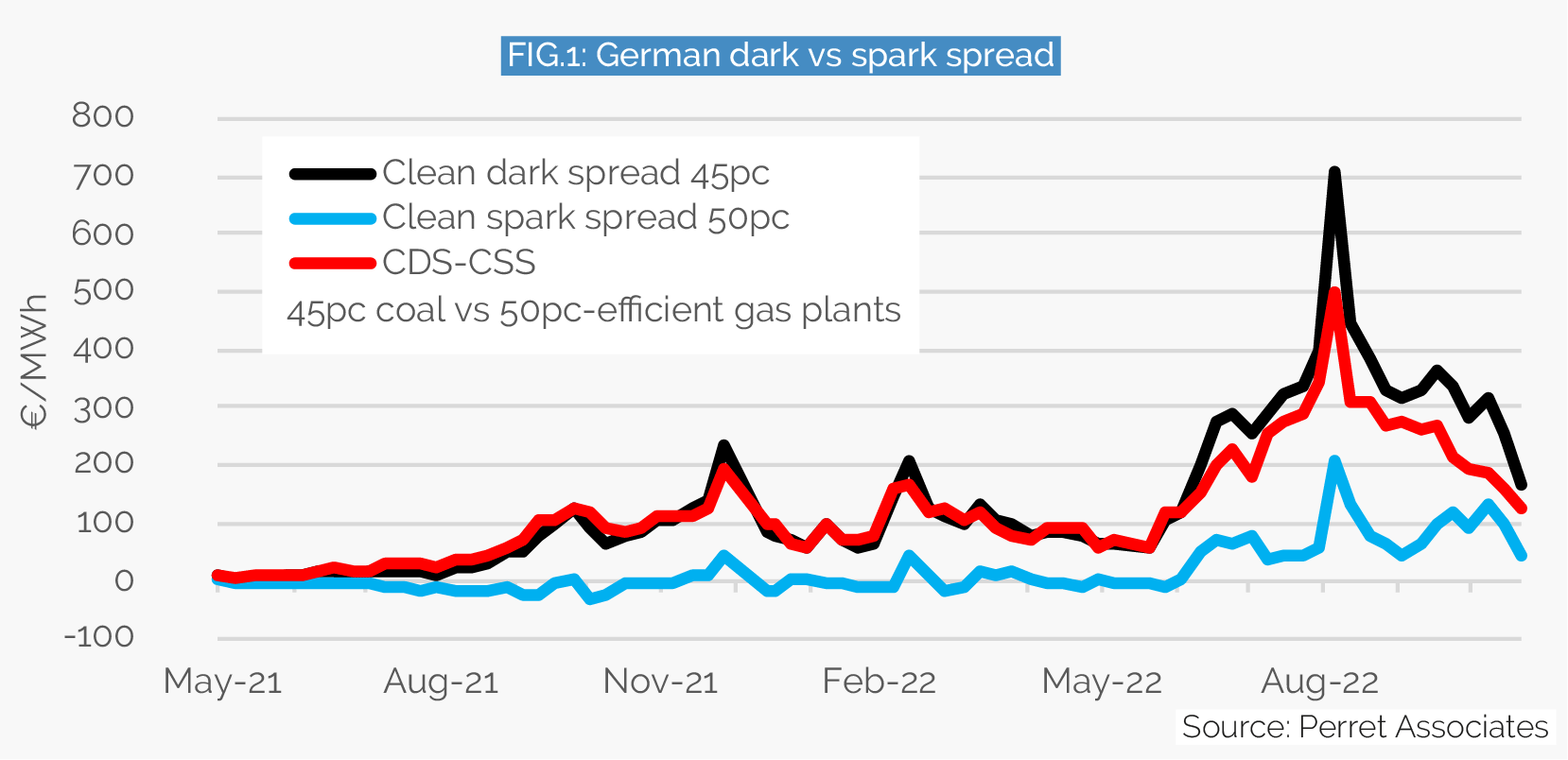

Indeed, coal has remained deeply competitive for electricity generation, based on forward prices for 2022, 2023 and even 2024. At the time of writing, the clean dark-spread (profit from coal-fired generation) for the Q1 2023 contract was still at €257/MWh ($266/MWh), a level unheard of prior to 2021, and almost twice the historical average of €140/MWh since May 2021. Still, it was below the all-time high of €709/MWh reached on 26 August 2022.

Thanks to these significant margins, German hard-coal-fired generation increased by 42pc year-on-year during the period January–August 2022, to 35.3TWh, despite some constraints limiting coal consumption.

German utilities had planned to dismantle certain hard coal power plants in 2022–23, but they had to make a U-turn following the invasion of Ukraine. All of a sudden, they needed to hire qualified personnel to run the power plants and to manage the coal procurement, often having to bring back ex-employees from retirement. They also had to accelerate plant maintenance and order new equipment, which had not been replaced due to expectations of an imminent closure.

Meanwhile, European governments increased the pressure to secure energy supply from all fossil fuels, as it was clear that wind, solar, nuclear and hydro would not be sufficient to cope with European demand as a large proportion of Russian gas became unavailable.

Perret Associates estimates that, over March–October 2022, German utilities and most end-users in the world imported more coal than they could actually use. This resulted in a significant increase in inventories at Amsterdam-Rotterdam-Antwerp terminals, to 8.3mn t on 5 September. More broadly, Perret Associates estimates global coal stocks to have reached 560mn t as of 31 August 2022, the highest level since June 2016.

Load factor

Due to this increase in stocks, as well as coal use in Europe remaining stubbornly low despite positive dark spreads, coal prices dropped significantly in September and October. Some contracts challenged the $200/t mark in early November, down 43pc from their peak in late August.

Indeed, coal use at German power plants, instead of increasing as could have been expected with the start of the heating season, dropped even further. First, October was the warmest month on record in most Western European countries. The heating season truly started in November and at a slow pace.

Second, and in a rather surprising development, the gas market very rapidly went from being under-supplied during H1 2022 to over-supplied from September. In fact, the day-ahead TTF gas contract traded at negative levels for a few hours in October, as strong deliveries of LNG imported from the US more than offset the halt to Russian gas supplies via the Nord Stream 1 pipeline.

The day-ahead gas contract recovered to €50–70/MWh in early November, but even at these levels gas was competitive against coal. Utilities and end-users able to do so switched back from coal to gas at short notice, which decreased coal usage and the drawdown of coal inventories even further.

Perret Associates forecasts that German steam coal usage for power generation will reach 18.5mn t in 2022, up by 2.3mn t, or 14pc, versus 2021. This would represent a load factor of only 30.6pc, whereas the consultancy had expected a load factor of 60–65pc in the wake of the invasion of Ukraine.

On the other hand, Perret Associates expects German gas-fired generation to end 2022 at 54.7TWh, little changed from 54.9TWh in 2021, thanks to a recent rebound in gas usage.

Restocking

Still, we are not out of the woods, with the heating season just ahead of us at the time of writing. The bulk of the steam coal and gas that the EU will use during the winter of 2022–23 is of Russian origin. But a new game will start at some stage in H1 2023, as the EU needs to rebuild stocks for the summer, and even more crucially for the winter of 2023–24.

Assuming no softening of EU sanctions against Russia—even in the case of a ceasefire in Ukraine or some negotiations over the conflict, the EU will have to import coal from other suppliers such as South Africa, Colombia, the US, Indonesia and Australia—which have so far sold their material at a significant premium over Russian coal.

A lot will also depend on the availability of US LNG for Europe, bearing in mind that Chinese LNG imports dropped to 54.1mn t over January–October 2022, down by 23pc year-on-year. In fact, Chinese utilities had been reselling LNG during the summer of 2022. An easing of a Chinese zero-Covid policy could again boost Chinese LNG and coal imports in 2023.

The magnitude of recent events—such as the Covid crisis, the embargo on Russian coal and cuts in Russian gas supplies—has been such that they have thrown the market’s traditional seasonality out of the window. The traditional September–November rally took place in June–August, which used to be a quieter period. We think that macro events will continue to prevail over the usual seasonality in 2023.

Another significant development is the segmentation of the international coal market. This year will mark the end of the globalisation that started in the mid 1990s. The international steam coal market, which used to create and adjust to arbitrage between the top six exporting countries (Indonesia, Australia, Russia, South Africa, Colombia, US) is now segmented in two main sub-markets: countries that do not accept Russian coal, and the growing list of countries still importing it.

Peak coal

In any case, the historical advantages of coal—large availability even outside the top six exporting countries; affordability against very expensive gas; reliability against wind and solar generation—prevailed once more in 2021–22.

Perret Associates have further delayed its peak coal scenario to 2025 and forecasts seaborne imports to still reach 860mn t in 2035, down by only 12.8pc from 2021’s levels. The consultancy also expects countries such as China to take the lead in the development of carbon capture, utilisation and storage technologies, while the EU bloc will accelerate its focus on wind and solar.

Over the last 300 years, the winning economies have been those able to use large quantities of cheap energy. However, we will know which countries have taken the correct decision in terms of recent energy policies only in 20 years’ time.

Guillaume Perret is the founder and director of the market analysis and research company, Perret Associates.

This article is part of our special Outlook 2023 report, which features predictions and expectations from the energy industry on key trends in the year ahead. Click here to read the full report.

Comments