Crude prices have held remarkably steady this year, but the calm will not last. In the coming year, oil prices may swoon amid oversupply. But far more certain and portentous, market participants are likely to radically shift their medium-term views from peak demand by 2030 to continued demand growth and, consequently, structural tightness. Investors should position for one of the most promising opportunities in a generation: acquiring the physical and financial assets that a growing world will continue to require for its prosperity and security.

Swoon before the boom

Rapidan Energy Group and others see oil prices coming under pressure next year as supply exceeds demand. If surpluses emerge, either OPEC+ or sanctions must reduce supply; otherwise, prices will fall until high-cost producers, especially US shale, pull back.

Any near-term glut will fade, but a deeper realisation will endure—the industry is underinvesting for the future.

Lessons from the last oil shock

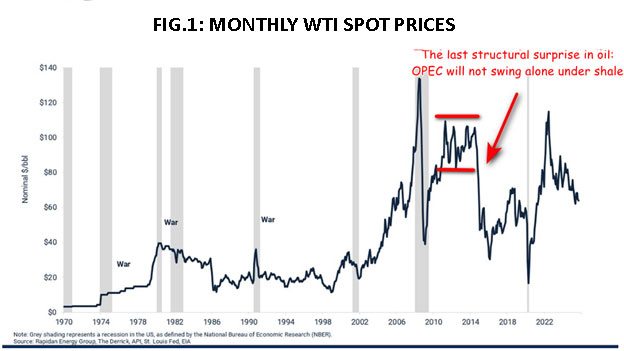

To grasp the scale of the coming unexpected structural realignment, recall the last one in 2014–16, when crude abruptly collapsed by 75% after years of $100/bl stability. Prices did not crash for the usual reasons—an economic downturn or sudden opening of the taps by Saudi Arabia. Instead, an unexpected event shattered the market’s confidence in a core assumption embedded in consensus outlooks: that OPEC alone would surrender market share under soaring US shale production.

The turning point came at OPEC’s 2014 Thanksgiving meeting, when Russia refused to join proposed cuts to offset shale growth. OPEC responded by keeping quotas unchanged, shocking traders who assumed it would defend prices, as OPEC and its predecessor swing producers had since 1932. Prices collapsed and kept falling until Russia joined OPEC+ in 2016, restoring some supply discipline.

Today’s consensus rests on an equally faulty premise that will soon disappear—this time, about demand. The belief that climate policies will drive a global oil demand peak around 2030 remains central to market thinking, but it is eroding rapidly. As the data disproves it, the fallout will be dramatic—bullish rather than bearish, unfolding over years rather than months. Unlike 2014’s bearish shock, which immediately pressured crude prices, the approaching demand shock presents a more medium-term investment opportunity in upstream and downstream oil assets.

Mesmerised by the peak-demand mirage

In recent years, most long-term forecasts have assumed global oil demand will decouple from GDP and peak around 2030, driven by strict climate policies, rapid EV adoption and extraordinary efficiency gains. The unprecedented “peak demand” narrative gained traction in 2020, when activists pressured the IEA to drop its policy-neutral reference case—once the benchmark for continued demand growth—and publish only policy-driven peak-demand scenarios.

The strategy to limit investment in oil supply by propagating a peak demand consensus worked: since 2020, upstream spending and discoveries have plunged, as a recent analysis by Rystad Energy confirmed. The oil industry is not investing nearly enough to meet global demand growth that will continue after 2030, when demand fails to peak.

Reality bats last and always cleans up

The world that nurtured those peak demand assumptions no longer exists. Low interest rates, stable geopolitics, cheap oil and open trade have given way to inflation, conflict, tariffs and energy-security concerns. Critically, the Western world prefers to decarbonise more slowly, through domestic manufacturing and supply lines, rather than to do so rapidly with cheap Chinese kit. Policy support for EVs is weakening across the US, Canada, Europe and China.

Meanwhile, the data are undermining the peak-demand thesis. OECD fuel consumption remains resilient instead of collapsing as peakists predicted: gasoline demand has reached multi-year highs in the UK and Spain. Efficiency improvements in internal combustion engines are modest instead of extraordinarily high.

BP, Equinor, McKinsey and other forecasters are already pushing their peak-demand estimates further into the future. Most notably, according to a Bloomberg News report by Javier Blas, the IEA will reintroduce a policy-neutral reference case in its forthcoming World Energy Outlook, showing continued oil demand growth through 2050. For the first time in five years, the world’s most influential energy forecaster will project that, under current policies, oil and gas demand will rise indefinitely rather than peak imminently.

Rapidan Energy Group never bought the peak demand narrative. Our long-term model’s base case projects that global oil demand will rise steadily through 2050. We model alternative scenarios with faster EV adoption showing a possible plateau in the 2040s—but only through consumer choice, not mandates or subsidies. Just as personal transportation shifted from horses to engines 125 years ago through innovation and consumer choice—not a ‘peak horse’ policy—technology and preference, not mandates, will likewise drive the next energy transition.

Buckle up

As the mirage of peak demand disappears, the depth of supply underinvestment will become clear. Discoveries and exploration spending have collapsed, decline rates are steepening and shorter-cycle US shale is maturing. OPEC+ spare capacity is more likely to peak by 2030 than global demand is.

As expectations shift towards structural tightness, prices will rise to draw capital back into the oil sector. The question is whether that adjustment will be orderly—funding timely reinvestment—or chaotic, fuelling another boom-bust cycle.

Robert McNally is president of Rapidan Energy Group. This article is taken from our Outlook 2026 report. To read Outlook in full, click here.

Comments