Pure-play UK producers are touting the relatively low carbon intensity of North Sea oil as a selling point in the shift to a lower carbon and, eventually, net-zero world. They are also looking at their Norwegian counterparts, who are posting even lower figures for kg CO₂/bl of oil produced due to power from shore—generated by renewables—rather than more greenhouse gas (GHG) intensive gas-fired turbines on the offshore production facilities themselves.

What these producers are not, though, largely talking about is scope three downstream emissions. They are preferring to focus on reducing the scope one and two emissions from their extraction and production of hydrocarbons and any scope three emissions arising from their upstream activities.

This is hardly surprising. For one, once they have sold their production they will likely have little or no visibility on what happens to it next. Linked to that, they have little ability to influence the evolution of this downstream scope three emissions number, so risk becoming hostage to a target out of their control.

“There is a lot of attention being focused on what is the GHG intensity of extraction, of scope one and two emissions,” agrees Kevin Birn, head of GHG estimation and coordination at data firm IHS Markit. “And the producers have gone there instinctually because, I think, this is an area they have the maximum control over because that is what they emit.”

Perhaps most importantly, there is no agreed methodology for tracking and verifying the emissions of the lifecycle of a barrel of oil—albeit operators can get high quality data for parts of the process under their control. Nor is there any clear idea of who will take responsibility for what emissions or how that responsibility might be spread across the value chain.

“Part of the challenge, even before you can get to who might account for what emissions, is that we are still at the point, when we look at emissions disclosure on a corporate level, where there is not sufficient coordination to be able to do a comparative analysis between the companies yet,” says Birn. “They are choosing to report slightly differently. We see different units of measurement. We see different emission boundaries within the minutiae.

“The first step, I think, is to get comparability, even at the scope one and two levels, to be able to do that comparative analysis and so we can understand what emissions look like. Once you get there, secondary questions about, say, double counting become somewhat easier because we have at least drawn the boundaries similarly around the sets of emissions that can occur.”

But, even with this lack of standardisation currently hampering public understanding, Birn does not think it is too early to start considering a future where the lifecycle of an oil barrel’s scope one to three emissions should be accounted for. “People are making business decisions based on this information, as incompatible and inconsistent as it is,” he says.

“Financial companies are changing their portfolios, they are buying and selling assets. We have got active divestment campaigns against some asset types. I am not sure the data is always comprehensive enough or the analysis consistent enough to provide complete answers, but, at the same time, that is not stopping decisions being made because the pressure to act is so great.”

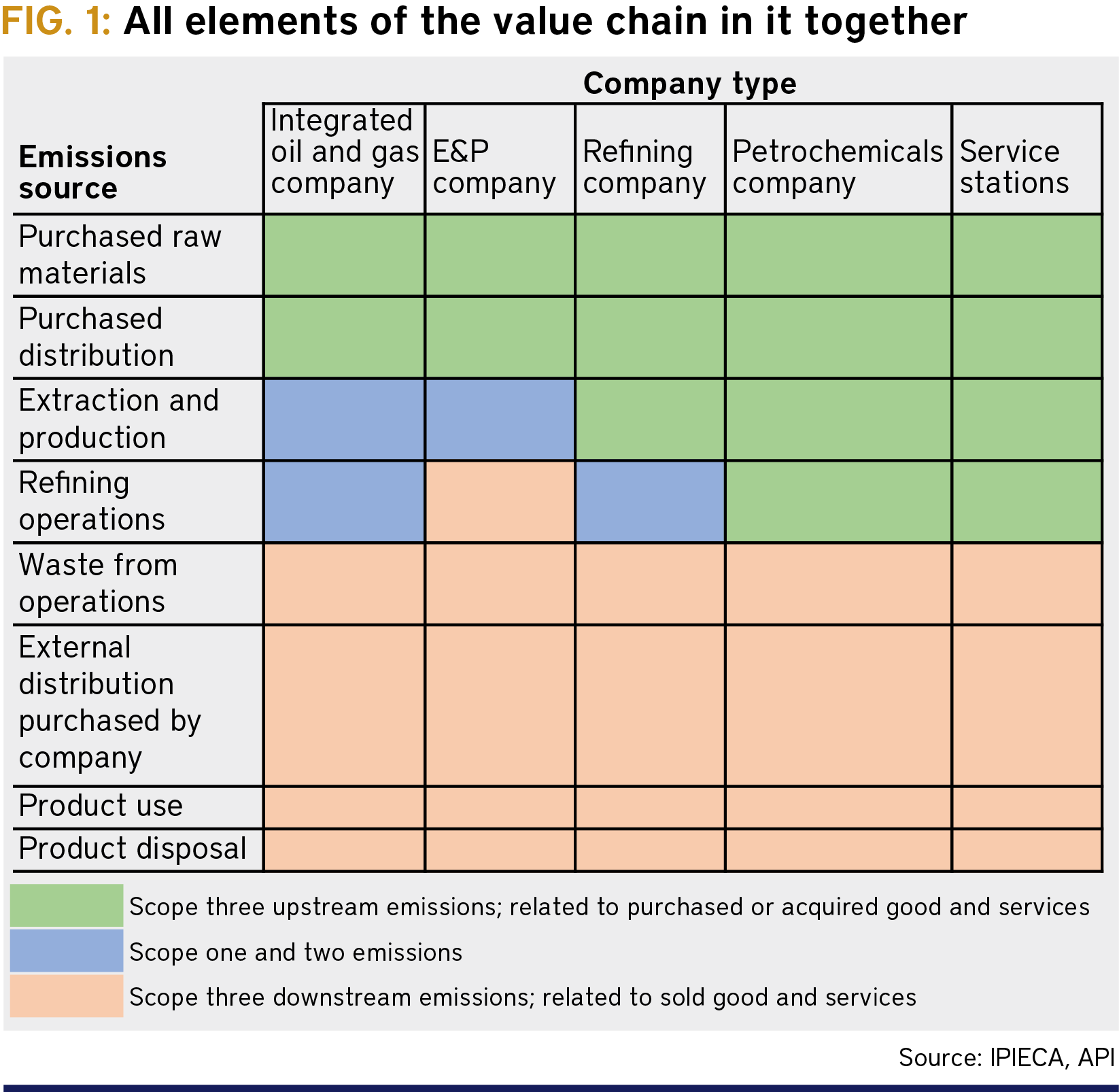

Work by the London-based oil and gas industry environmental and social performance lobby group IPIECA and the US’ API dating back as far as 2016 suggests, though, there is an understanding that all elements of the chain—be they independent producers, refiners or petrochemicals firms and distributors, or integrated companies that fulfil more than one or all of these functions—are on the hook for scope three emissions (see Fig.1). What needs to be thrashed out is how those responsibilities will be assigned.

There are several elements to get right. One is to avoid a particular market segment being saddled with too much of the burden.

Independent oil producers may like the idea of abdicating responsibility as soon as a cargo is sold. But if, say, refining is held responsible for all emissions that result from a barrel once it is beyond the upstream stage, we might expect to see a mass exodus of integrateds from the sector, a collapse in its investment case and a hugely disorderly outcome.

That is not to say that measuring at the refinery or petchems plant level might not be the best logistical solution, as it could capture the complexity of different crude grades—with varying carbon intensities—going in and the slew of refined products, petchems and feedstocks for additional processing coming out. To some extent, this could mirror the current EU emissions trading scheme, which considers CO₂ release on an individual installation level.

These measured carbon footprints could then be allotted to the various players in the chain according to agreed parameters. Such a solution could also tackle what will be one of the inevitable challenges, namely double counting.

Overlap

It is all very well activist investors demanding that a major such as Shell sets binding targets for its scope one, two and three emissions. But what happens when Shell’s emissions from, say, a process at one of its refineries overlaps with players both upstream and downstream of its activities?

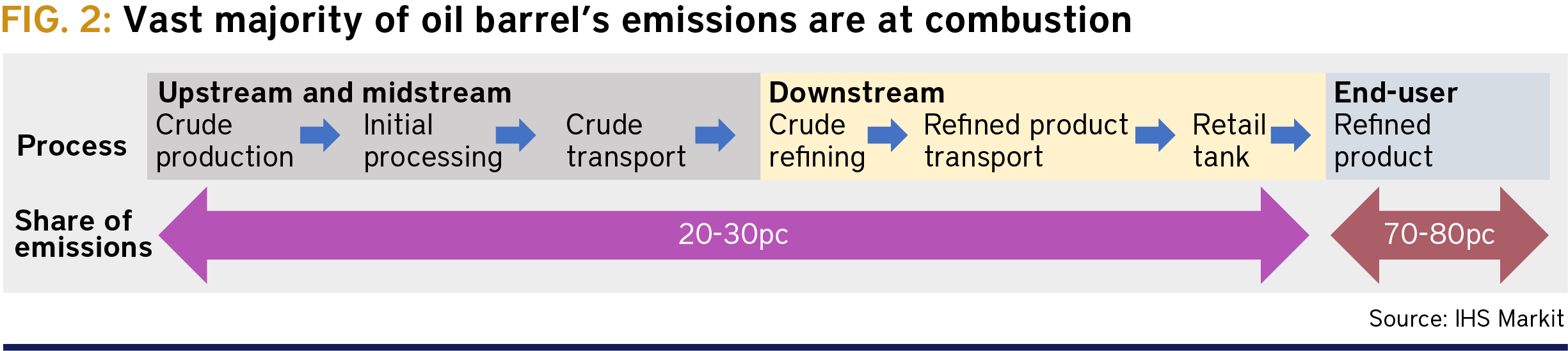

Another vexed question is the appetite of the end-user to participate in bearing any responsibility for the carbon footprint of products they consume. This gets to one of the thornier issues in the debate—upstream production and downstream refining accounts for only c.20-30pc of the carbon footprint of a barrel of oil, according to IHS Markit (see Fig.2). The vast majority, c.70-80pc, of the CO₂ emitted, is in the combustion phase, by industrial end-users and transportation firms, but also by individuals.

Shell’s social media suggestion last year about the need for potential changes in consumer behaviour sparked a significant backlash—with accusations of ‘gaslighting’ and outrage that fossil fuel companies could even suggest the problem was not them but might be shared by those that ultimately use their products.

The Anglo-Dutch major still seems slightly bemused that, as an energy supply firm, it might also be responsible for shaping consumer demand for energy. That ‘it is all the oil companies’ fault’ attitude suggests that the general public—other than having the cost of these production-to-combustion emissions passed on to them in the retail price, as they already do in, for example, US and European biofuels mandates—will play no direct part in the process.

On the other hand, airlines have, for a number of years, been offering passengers the option of offsetting the carbon footprint of their flights. This could point to a model where consumers are prepared to play a more dynamic role in interacting with the emissions of any fossil fuel-derived products they use.

Comments