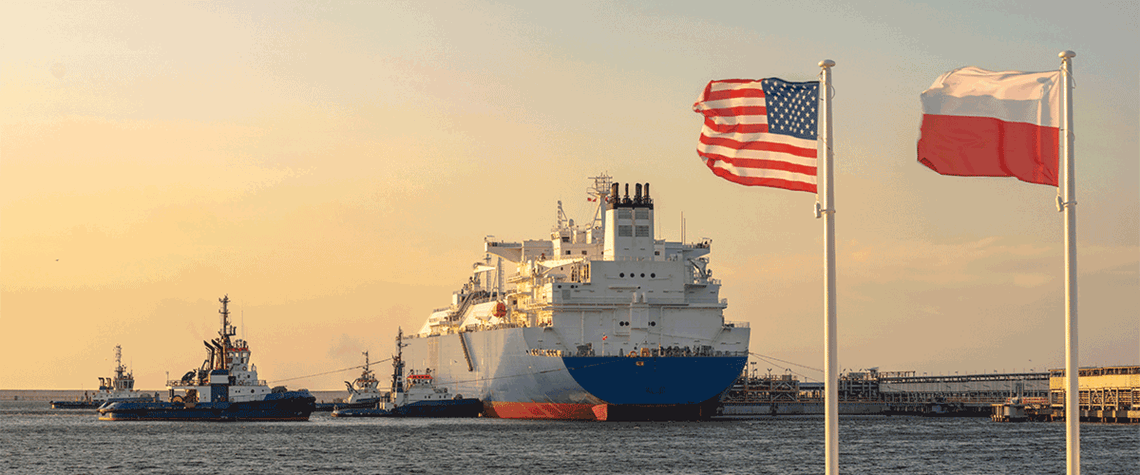

US has gone from being an importer of gas to being the largest supplier of LNG

Global LNG analysis report 2023 – Part 4

The fourth and final part of this deep-dive analysis looks at LNG projects planned or underway across the Americas

Global gas demand is being by short-term and long-term factors including the energy transition and the war in Ukraine. The first three parts of this report covered liquefaction and regasification projects in Africa, the Middle East, Asia and Europe. This fourth instalment examines North and Central/South Americas. Most notably within the region, the US has transformed itself from being an importer of gas around a decade ago to being the largest supplier of LNG in the world. North of the border, Canada has had less success in progressing its projects, with only a small number likely to push ahead to completion. Meanwhile, in Central and South America, Mexico remains the most significant count

Also in this section

28 April 2026

Oil traders warning of $200/bl oil are wrong, and the market should be wary of proclamations that the impact of the oil shortage has only begun to be felt and a that a ‘harsh adjustment’ is coming—even for industrialised nations

28 April 2026

Restoring supply from Saudi Arabia, the UAE, Kuwait, Qatar, Bahrain and Iraq involves complexities far beyond simply adjusting operational controls

28 April 2026

Datacentres will guzzle power at a ferocious rate, but the impact on wider energy markets will be far more complex than previously thought

28 April 2026

The key energy player faces balancing regional routes, political complexities, and creating a clear strategic vision for energy security