With critical minerals having emerged as the indispensable building blocks of the clean-energy economy, developed countries are forming a web of alliances to diversify supply chains away from China’s dominant role in mining, processing and refining.

ASEAN sits at the centre of both opportunity and risk. The region’s mineral wealth and processing potential make it a natural diversification hub. During his recent Asia trip, US President Donald Trump reinforced this effort through new agreements touching on critical minerals cooperation with Malaysia, Thailand, Vietnam and Cambodia, underscoring the region’s growing role in global supply-chain realignment. Yet resource nationalism, fragmented regulation and the region’s deep energy trilemma—the struggle to balance energy security, affordability and sustainability—continue to complicate this ambition.

Limits of diversification

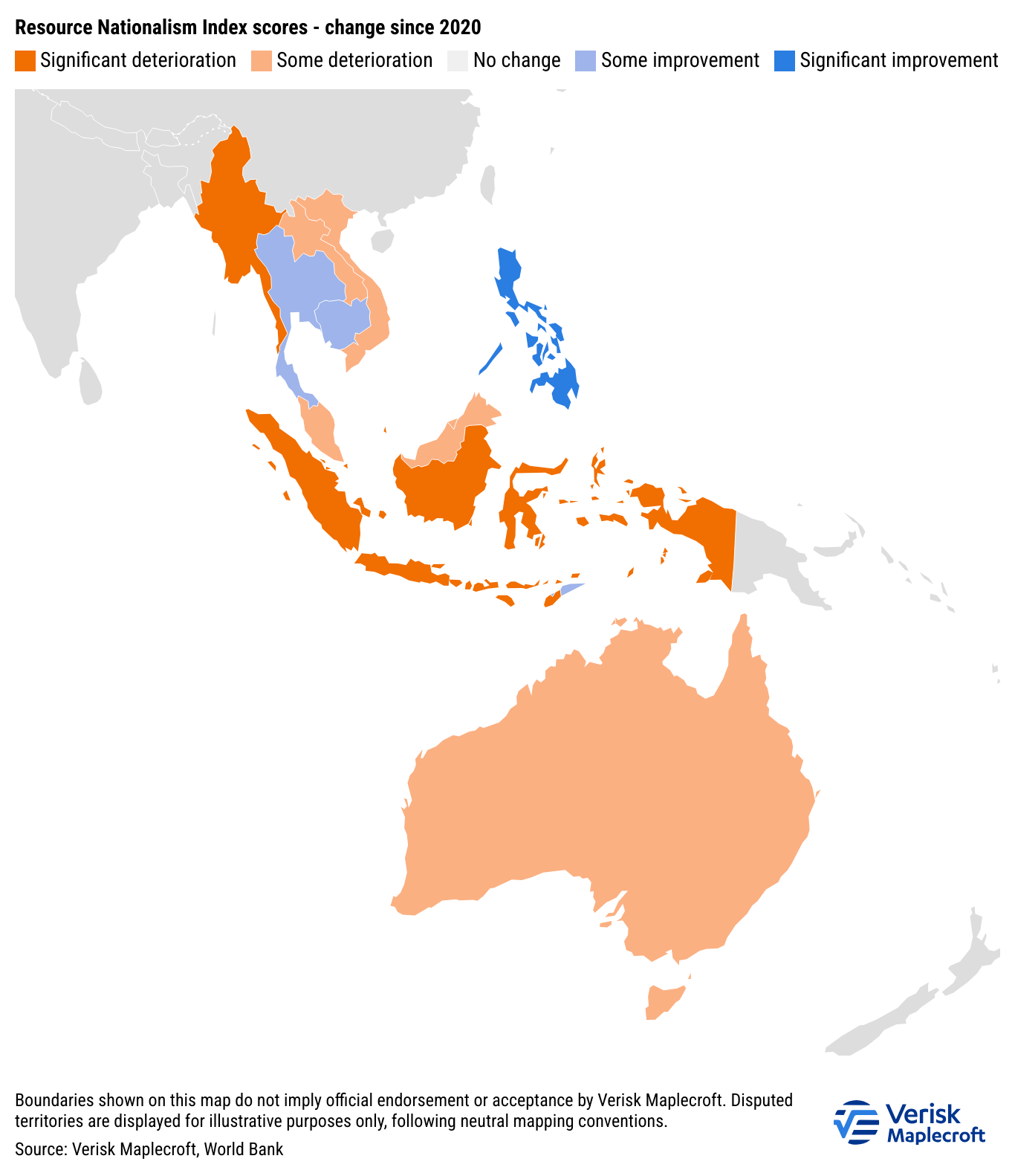

Positioning ASEAN as a diversification strategy is fraught with difficulty. The challenge lies not only in locating alternative resource bases, but also in navigating rising resource nationalism and institutional fragility within producer countries. Verisk Maplecroft’s data show that most ASEAN economies have seen an increase in risk on its Resource Nationalism Index since 2020, reflecting a growing tendency towards critical mineral protectionism.

Indonesia and Malaysia are prime examples of this trend. Indonesia, which possesses some of the world’s largest reserves of nickel—a key input for electric vehicle batteries—has repeatedly imposed and lifted export bans on unprocessed ore to compel foreign investors to build domestic smelters and battery plants. A 2014 ban was lifted in 2017, then re-imposed in 2020, and similar restrictions are being considered for bauxite, cobalt and tin.

Malaysia, an emerging processing and refining hub, has also introduced intermittent export restrictions on raw rare earths and other mineral resources to prioritise domestic downstream development. Even countries showing improvement on the Resource Nationalism Index—such as the Philippines, where export restrictions on nickel ore were previously considered—have toyed with the idea of replicating Indonesia’s downstream model.

In essence, governments are increasingly utilising mineral resources as instruments of industrial strategy and national revenue generation. This is even seen in the most promising critical minerals markets, where frequent policy reversals, opaque licensing and weak sustainability standards discourage long-term investment and undermine regional supply stability. Divergent policy priorities could undermine efforts to coordinate regional supply chains of critical minerals. Other potential APAC producers, including Myanmar and Cambodia, face even greater challenges from political instability, limited infrastructure and inconsistent regulatory enforcement.

Energy trilemma suppressing critical mineral alliances

Western-led critical mineral alliances are colliding with Asia’s enduring energy trilemma. While these partnerships aim to stabilise mineral flows for clean technologies, producer countries face competing domestic priorities that reshape how these goals are pursued in practice.

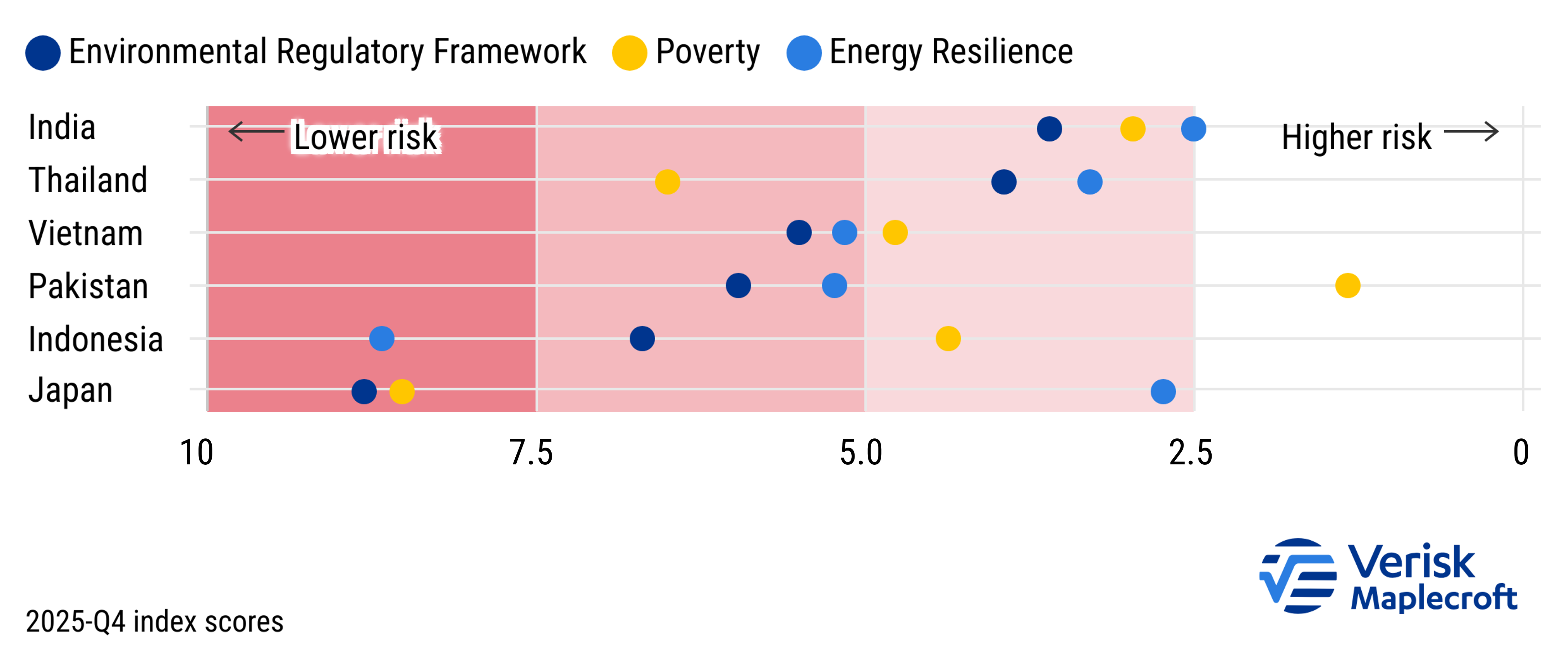

Across the APAC region, the energy trilemma is intensifying. Verisk Maplecroft’s Country Risk Data shows that no major Asian economy—whether emerging or advanced—is considered lower risk for energy resilience, poverty and the strength of their environmental regulations simultaneously. Every one of these markets is assessed as higher risk for at least one of these issues. Even advanced economies such as Japan, South Korea and Singapore remain vulnerable to import dependence and price volatility, while emerging economies—including Indonesia, Vietnam and India—struggle to balance development needs with decarbonisation.

The energy trilemma has become the fault line of critical mineral alliances in the APAC region. Exporters guard resources to secure domestic value and jobs, while importers seek diversification through new partnerships—but both are constrained by rising transition costs.

Efforts to secure minerals for the clean energy transition risk being undermined by the same affordability and development priorities driving resource nationalism. Unless regional cooperation evolves to reconcile these competing goals, critical mineral partnerships may reinforce fragmentation rather than deliver true supply resilience, leaving Asia’s energy transition more interdependent, yet no less uncertain.

APAC’s fragmented transition outlooks

In the coming years, protectionist measures and state intervention are likely to intensify, driving further fragmentation across critical mineral and renewable energy markets. At the same time, Western economies are expected to tighten trade and investment frameworks, using stricter sustainability standards and ‘friend-shoring’ incentives to secure supply chains while managing exposure to strategic competitors. For ASEAN economies, the key challenge will be to convert mineral endowments into durable industrial capacity while remaining integrated within global value chains.

Achieving the balance between domestic development objectives, energy security imperatives and external partnership commitments will be central to shaping a more stable and sustainable trajectory for Asia’s energy transition.

Kaho Yu is head of energy and resources research and Laura Schwartz is senior Asia analyst at Verisk Maplecroft. This article is taken from our Outlook 2026 report. To read Outlook 2026 in full, click here.

Comments