It is easy to forget that, pre-Covid, new International Maritime Organization (IMO) 2020 regulations reducing the maximum sulphur content in much of the world’s bunker fuels from 3.5pc to 0.5pc were expected to be one of the dominant narratives in the year’s oil price dynamics.

The demand hit in the wake of pandemic’s global restrictions has, as well as eclipsing IMO 2020’s significance, also dampened its impact, as anticipated pressure on supply has been greatly reduced. Nonetheless, the effects are being felt—if more in the background than might have been expected.

Story so far

Among the most notable observations as yet, supply of very low sulphur fuel oil (VLSFO) has proven more than adequate, while the call on marine gasoil (MGO) as an expensive alternative has been less than expected.

Refiners have adjusted their crude sales and changed their blend component pools. And many have strengthened their direct position in the bunkering markets with their own—sometimes proprietary—blends of VLSFO.

Competition for low sulphur heavy gasoil and waxy streams has increased, which has generated a revival in hydroskimming economics. And low sulphur vacuum gasoil (LSVGO) has become a reference both for cracker feedstock pricing and for bunker economics.

Supply of other alternative fuels continues to be developed, most notably LNG—the fastest-growing and most scalable—with supply infrastructure expanding steadily. But these fuels, which also include methanol and ammonia, will act chiefly to achieve the targets set out in the IMO 2050 decarbonisation agenda

On the other hand, scrubbing economics continue to hang in the balance. It is our expectation that scrubbing as a technology will be no more than a short-term solution, as shipowners switch to cleaner fuel alternatives.

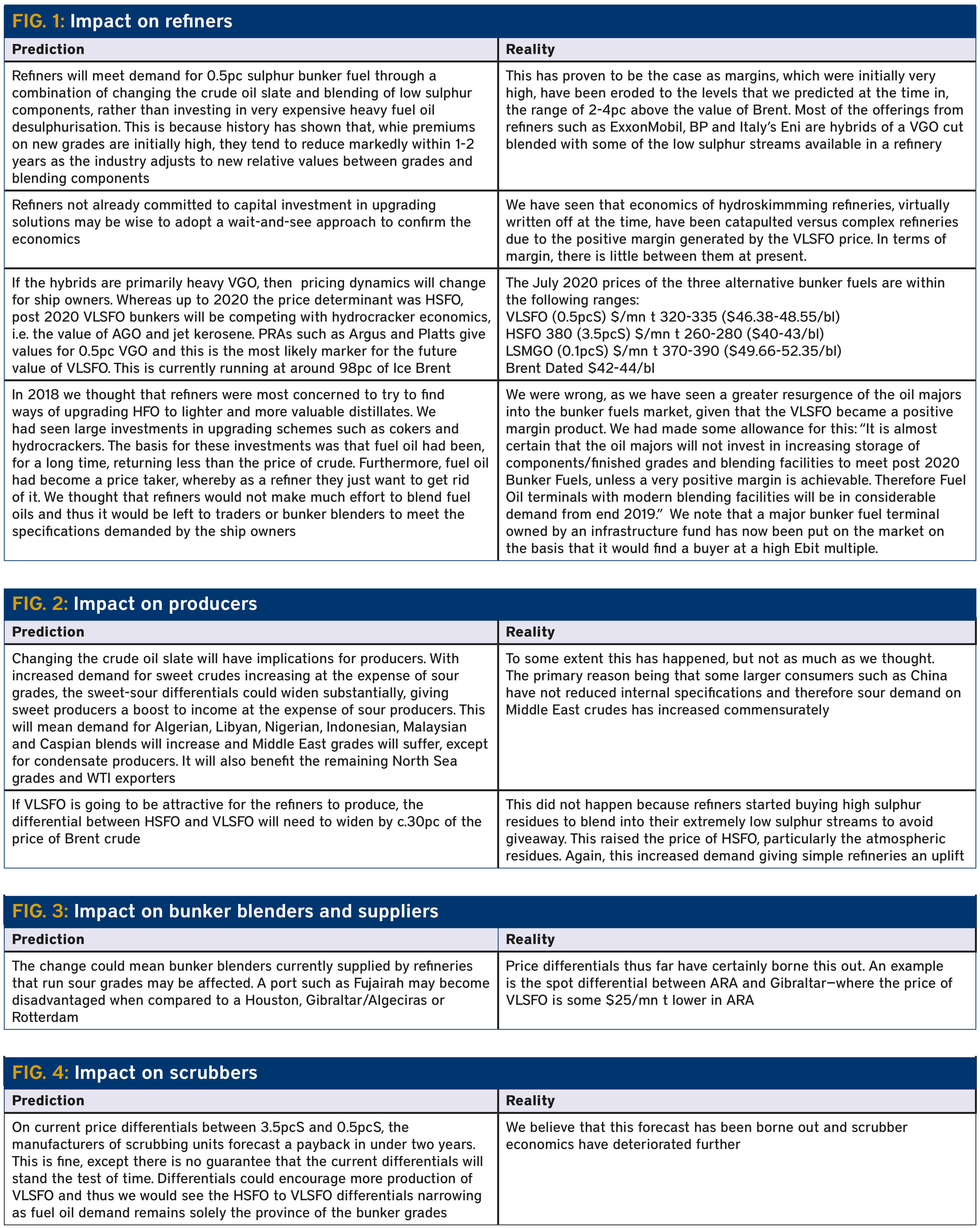

Channoil revisited some work it did in 2018 on potential IMO 2020 impacts and looked in some depth at what it got right and wrong on the potential implications for various types of stakeholders compared with what we have seen so far (see Figs. 1-4).

Moving forward

Less than eight months in, and a highly unusual eight months at that, the IMO 2020 story is far from over. We must also look ahead to what might happen next. The outlook for fuels and distillate prices is confused due to a number of ‘known unknowns’, including:

- Uptake of renewable fuels

- Uptake of electric cars and their impact on power generation

- Potential impact of carbon capture and storage

- Growth in coker investments

- Growth in LNG/LPG/methanol as bunker fuels

- Impact of incompatibility within new blended fuels

- Potential for cheaper scrubber technology

- Other technological breakthroughs

- A realistic price setting for carbon emissions.

But there are certain observations we can offer on some of these uncertainties. For one, the price of solar and wind continues to decrease steadily. Coupled with the increase in battery storage technology, this has put the renewable argument to the fore. The cost of hydrogen production is also plummeting and—due to a likely surge in the availability of cheap renewable power—electrolysis is making hydrogen power a realistic contender for the fuel crown.

Forecast growth of electric and hybrid cars also continues to push further upwards. The effect of 1mn electric cars—assumed by 2035—is to reduce crude oil demand by 1mn bl/d. But we are conscious of the fact that, in developed economies, carpools are rotated every seven years. If the fashion for electric cars accelerates, then that timeframe could get rapidly shorter.

European governments, for example those of France and the UK, have also set policy goals to reduce the number of diesel cars. A big reduction in diesel engines will have an immediate effect on the price of middle distillate. If coker investments carry on, then it is possible to imagine a scenario where the differential between diesel and HFO will narrow.

The use of marine gasoil (MGO) in engines has not increased as rapidly as we thought, perhaps as ship engineers still think in terms of volume ($/t) rather than energy content ($/mn Btu). There is also a lubricity argument in favour of higher viscosity fuels, while low viscosity MGO needs cooling before it enters the engine and thus, if VLSFO is available, it is more ‘engineer acceptable’. But the question will arise again once NOx and PMO specifications are tightened further.

Charles Daly is founder and chairman of international oil and gas consultancy Channoil.

Comments