Oil is not alone in reeling from the impact of the Covid-19 pandemic. Virtually every industry in every part of the world is adversely impacted by the crisis in the world. In addition, near-total lockdowns are causing further complications both to national economies but also to global supply chains and trade.

The resulting drop in end-consumer demand for oil has led directly to excess supply and, in turn, unprecedented stock builds and spectacularly low—even negative—prices. Even the most comprehensive ever supply-side agreement between Opec+ and various other producing countries, to reduce supply from May onwards, is in grave danger of being ‘too little too late’ to bring supply anywhere in line with the new demand reality.

Capex focus

Strategy consultancy Simon-Kucher recently conducted a survey [1], in collaboration with Houston’s Rice University, with oil industry executives to understand their pain points, strategic agenda and potential mitigation strategies during the current price downturn.

The key messages the survey returned were:

- Companies are focused on cutting their capex by up to 30pc in the near-term

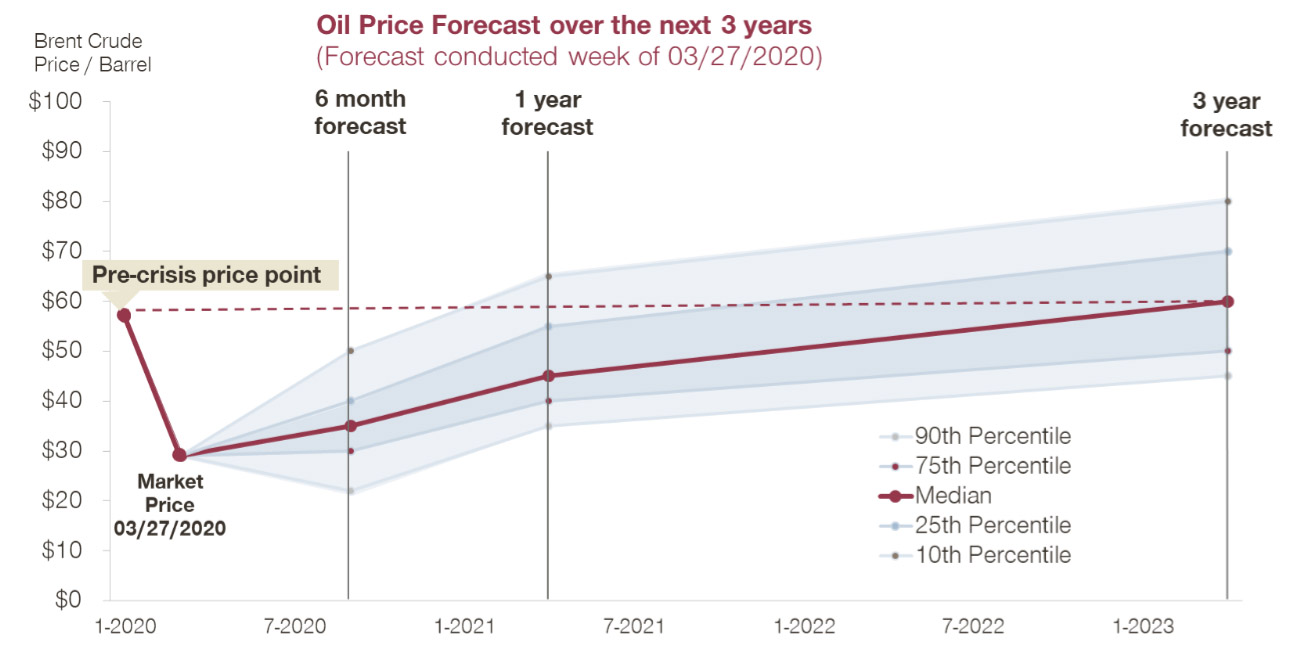

- It could take up to 3 years for Brent to go back to $60/bl

- The new focus will be on operational efficiency and capital use, rather than on top-line growth

Ignore price at your peril

Oil executives realise that initiatives on the pricing of their product yield the highest ROI, but they are under-investing in pricing projects and focused on cost cutting. One possible reason is that, despite that realisation, the industry still underestimates the true impact of pricing.

In short, the industry looks set to repeat a previously tested formula of cost savings to ‘hibernate’ through a price winter. However, based on Simon-Kucher’s 35-year experience of working on pricing in the energy industry, we are convinced that the prospect of negative price spikes will be a more and more frequent phenomena.

On the Epex trading venue for European power, for example, the number of hours with negative electricity prices has increased from 15 hours in 2008 to 211 hours in 2019. Last year, the power producer actually paid the ‘buyer’ a sum per megawatt hour for consuming their power for an aggregate of almost 10 days.

More widely, we see negative pricing occurring more and more frequently occurs in our daily lives, whether it is cashback for cars, negative interest loan or simply cash incentives to switch your bank.

Long road back

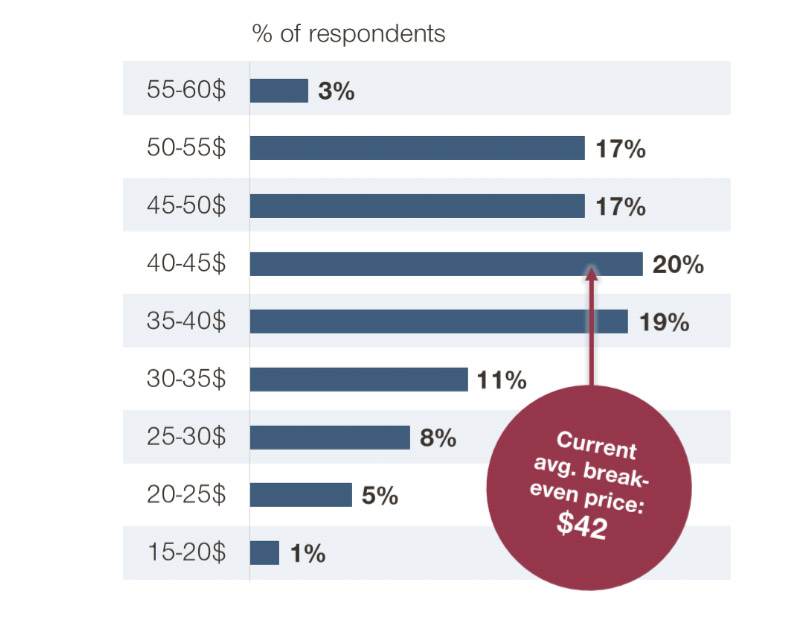

In the market study, the participants stated that their mean breakeven oil price was just above $40/bbl.

The median of survey participants also expected a period of three years until the oil price recovers to a level of $60/bl.

With significant continuing risk for short-term shocks that could take prices back down close to or even below zero and a long recovery period for the oil price, we recommend a different perspective. In short, we challenge the notion that oil companies will be able to lift themselves out of this crisis simply by cost saving. Instead, we recommend a set of topline measures.

Moving forward

We believe that oil companies should adopt the following key commercial and pricing decisions to counter the prevailing challenges:

Shy away from signing long-term customer contracts, especially with large customers

- Instead, push volume through spot transactions and to spot customers

Closely track and monitor the Brent crude price

- Leverage historical models to scenario plan and decide on the commercial strategy in each case

- Forecast models should be used—however, they may not be able to predict in all the scenarios

Focus on protecting market share with large customers

- Redirect volume from small or spot customers as needed to ensure supply and contractual obligations with large customers

Rebalance the customer mix between large, medium and small

- Take tactical and commercial steps to increase the balance towards large customers

Fix drops in volume through sales strategy rather than drops in price

- Prices should be linked closely with Brent crude

- But additional discounts or rebates will not arrest a slump in demand.

Focus on managing net working capital and cash

- Raising from the market will continue to be tough

- This temporary credit crunch will hit small and medium oil companies more than the large ones

Navigating through

Oil companies’ current tough time will likely get even worse across June and July 2020. It is imperative that firms take certain commercial decisions to manage the impact and future-proof themselves.

The industry has been facing an at least partially climate change-led downturn for a number of years. The current crisis on the back of Covid-19 is only accelerating and exacerbating the problem. Yet business models have not changed in a long time. We believe now is a good opportunity to do so, e.g. to implement digitalisation strategies.

To reiterate, oil companies cannot deal with this crisis purely through cost cutting. There is a limit to how much cost can be cut before the process starts to adversely impact the core business. Instead, oil companies should focus on commercial strategies, like pricing.

Andreas Jonason is a partner at Simon-Kucher in Stockholm, Kiran Pudi is a senior director at Simon-Kucher in Singapore. Florian Thaler is the CEO and co-founder of OilX in London.

Note: [1] https://www.simon-kucher.com/fr/node/5475: About the Study: The 2020 Oil & Gas Crisis Study was conducted by Simon-Kucher & Partners and Rice University between March, 27 – April 3, 2020 . Globally, 195 Oil & Gas executives from all major industry verticals were surveyed by Simon-Kucher and Dynata, an independent market research institute.

Comments