2023 has been an extraordinary year for Russian oil exports. Driven by Western sanctions, and in particular the phase-out of most European crude and product imports from Russia, the hydrocarbon superpower had to look for alternative outlets.

After all, and against the expectations of many, it was neither particularly difficult for Russia to find new buyers nor for Europe to procure replacement diesel and crude oil. And while the new equilibrium has a higher demand on vessel ton-miles, not even that was sufficient to boost freight rates to a permanently higher level.

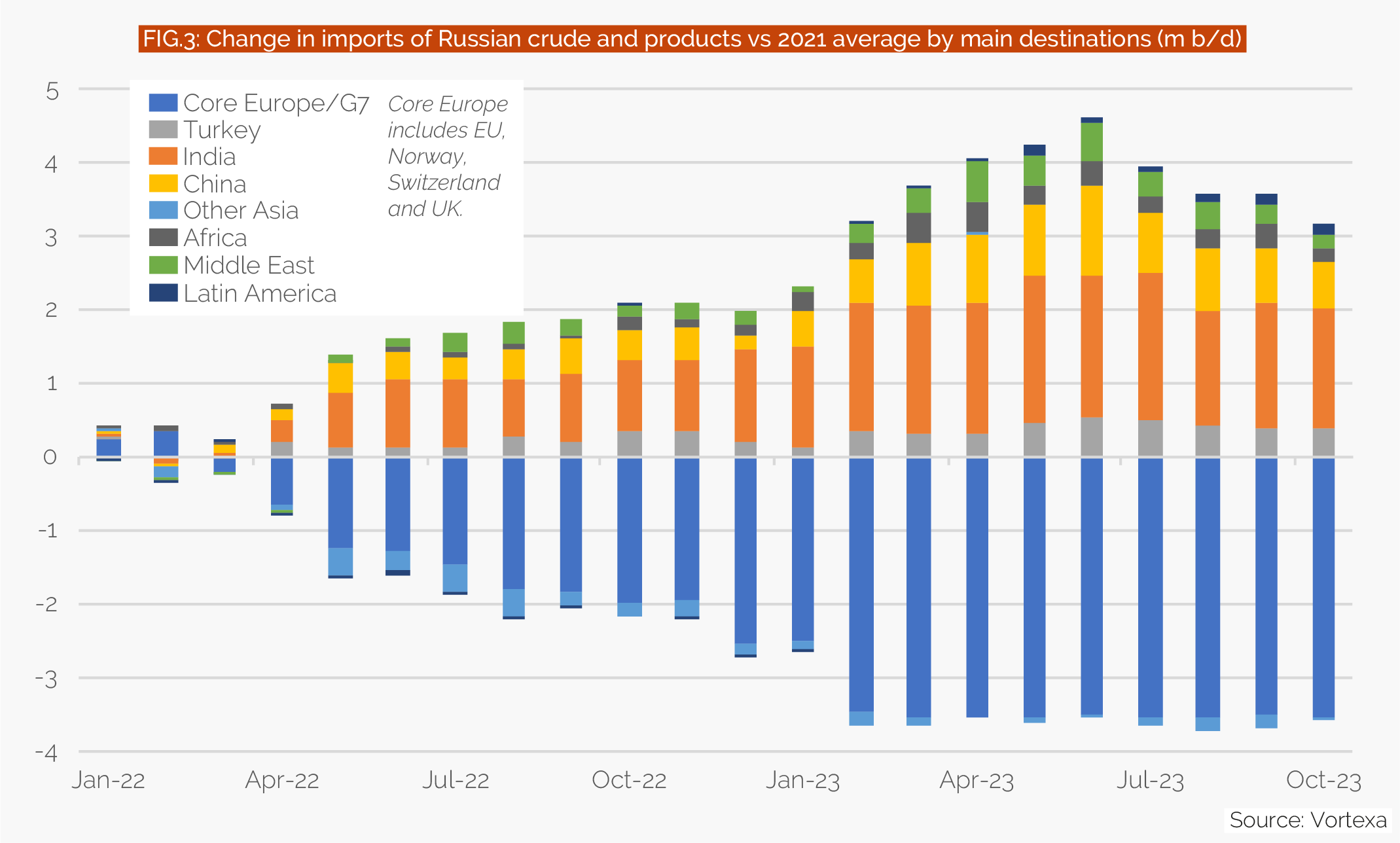

Russian oil flows in the new paradigm can be split into two phases. In the first six months of 2023, Russian arrivals in new destination markets hit steadily new record highs, facilitated by deep discounts. The staged European phase-out (first crude, then diesel) was completed in early February. Some initial hesitation on the buyer side in combination with the seasonal peak in Russian oil exports in March led to a peak in arrivals of Russian oil in new markets in the month of June.

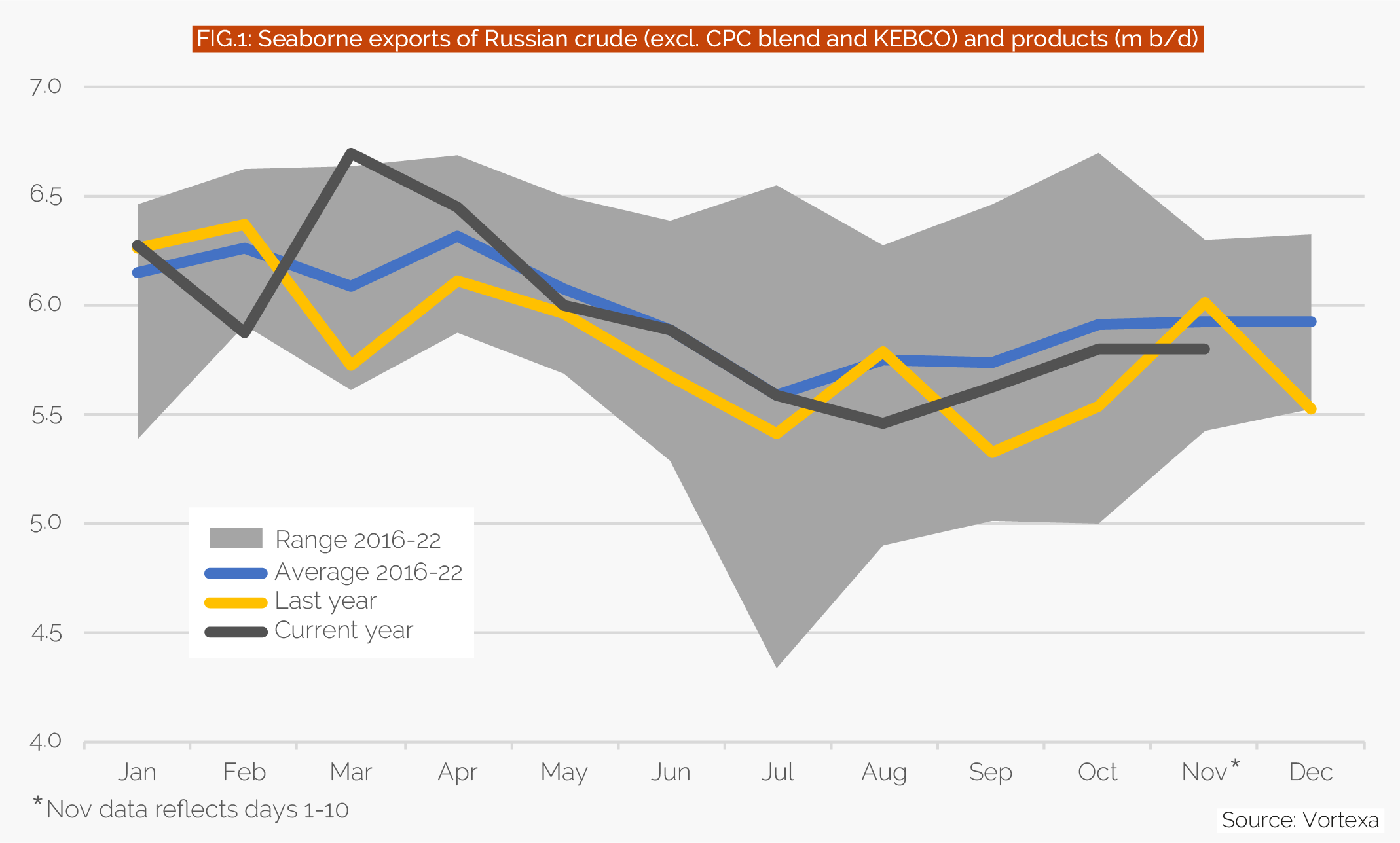

From that point onwards, flows and the stress on the logistical system were easing from various perspectives. As a key factor, seaborne exports of Russian crude (excluding CPC Blend and KEBCO, both transit grades from Kazakhstan) fell from an extraordinarily high 6.7m b/d in March to a low point below 5.5m b/d in August.

A superficial view on the massive 1.2m b/d gap would suggest that Russia must have curtailed supplies dramatically, having announced combined cuts of 1m b/d in crude exports for the month of August. But the truth is that the average seasonal decline in exports already accounts for more than 0.7m b/d of this. And March figures were just strongly inflated due to substantial delays in exports from February due to winter storms.

On average, January to July exports of Russian oil were perfectly aligned with the seasonal average, while over August to October a shortfall of some 250k b/d can be noted. This may well serve as a good indicator of the combined effects of the announced crude exports cuts in close alignment with OPEC+ and particularly Saudi Arabia, as well as the partial export ban on diesel and gasoline established in the latter part of September.

Slower Russian exports in H2 2023 tightened the market for these semi-sanctioned barrels, leading to higher prices. It is sometimes forgotten that it is entirely legal to import Russian oil for most countries outside the EU/G7 group, as long as no Western shipping, financing and other related services are used. Accordingly, a new fleet established itself over the course of 2023 and logistics became pretty fluent again, curtailing vessel utilisation beyond lower underlying volumes. Furthermore, fresh interest for Russian diesel from markets such as Brazil helped to keep somewhat shorter-haul barrels to the Atlantic Basin more stable, while the declines materialised in particular towards East of Suez markets.

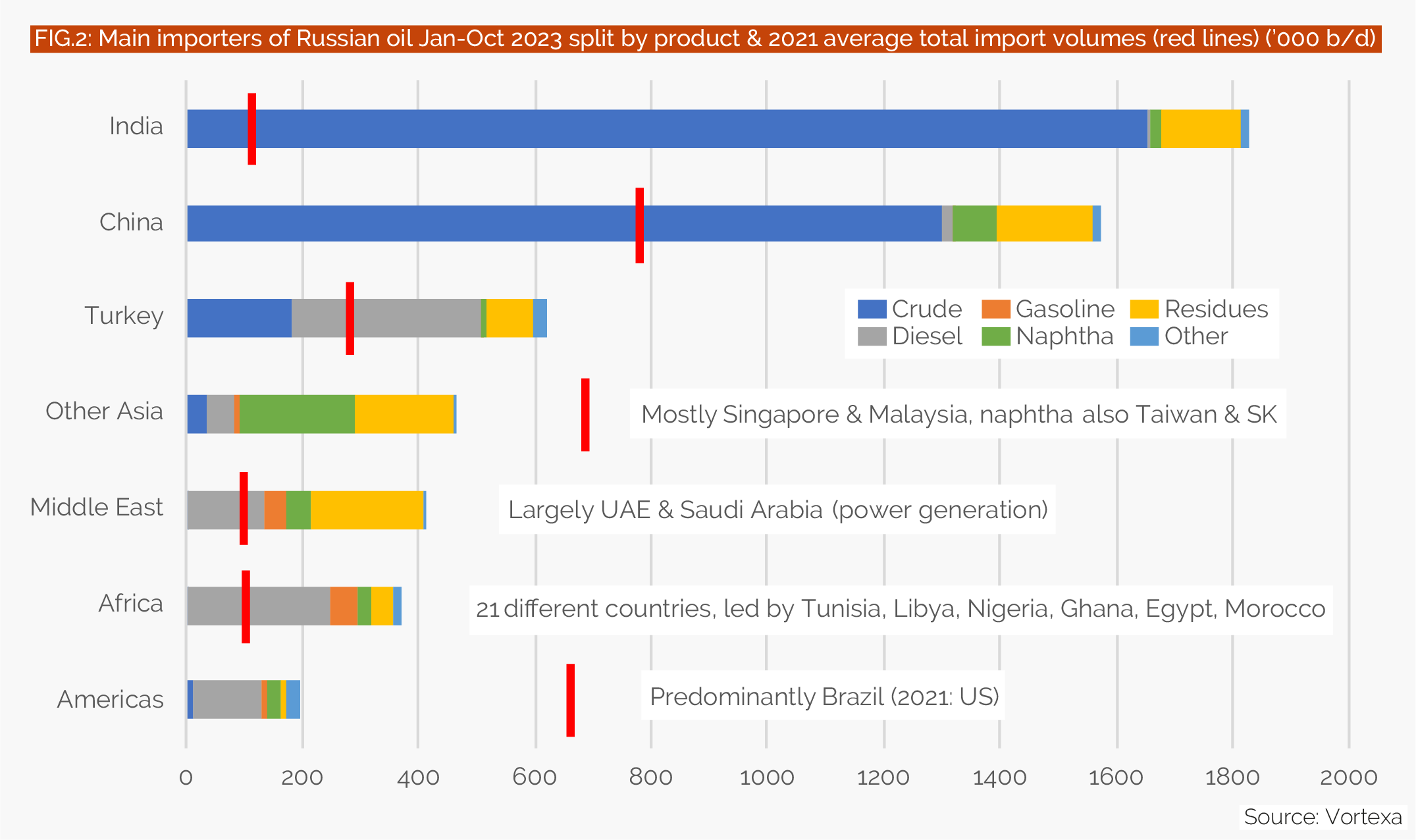

Nevertheless, India is clearly the number one opportunistic buyer of Russian oil. Up from negligible volumes in 2021, Indian imports of predominantly crude oil peaked at 2.1m b/d over May to June, before falling back to 1.7m b/d since then. But Chinese imports of Russian oil declined by 0.7m b/d from a June peak to an October low. Middle Eastern imports fell by about 350,000 b/d from peak to trough, with the end of the power generation season in Saudi Arabia playing a role.

Looking forward to 2024, two things are likely to happen. As domestic Russian oil demand eases over winter months, exports are set to rise by at least 0.5m b/d towards the usual peak in April. But competition for the Russian barrels, which are still offered at some discounts, will remain strong, and the recent marginal transition from East of Suez to West of Suez buyers may well go on.

Opportunistic buyers will have a harder time than in 2023 and logistical costs will play a bigger role. Buyers such as Turkey, North and West African countries and possibly more Latin American players are likely to increase their share in Russian oil further. Meanwhile in particular China may well see a further decline in flows, as it is simply too far away from the key Baltic and Black Sea ports. Only if some hiccups were to materialise in logistics, e.g. due to tightening sanctions, would China become more relevant again as a buyer of last resort.

But such hiccups are unlikely. Ultimately pretty much everybody in the market wants Russian oil to continue flowing, as otherwise massive price rises are unavoidable. Similarly, Russia itself will not deliberately forego crucial income in its war economy. And, as in 2023, any potential shortfall in the fleet transporting Russian oil will be picked up quickly by new players, with procurement prices of old vessels set to fall amid a reasonably long oil tanker market.

David Wech is the chief economist at Vortexa.

This article was published as part of PE Outlook 2024, which is available for subscribers here. Non-subscribers can purchase a copy of the digital edition here.

Comments