Lower gas prices have caused producers in gas-rich basins to scale back operations

US shale starts 2023 in ‘realistic’ mood

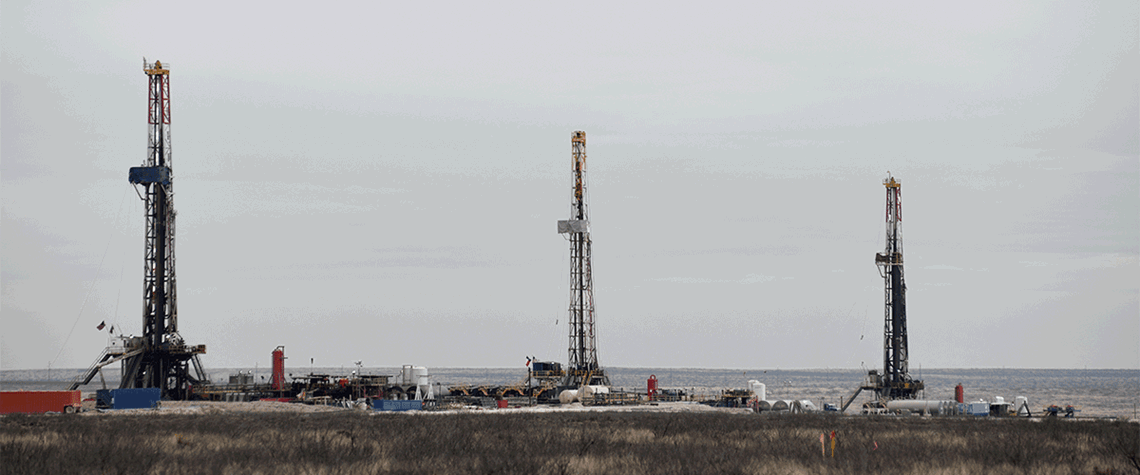

First-quarter shale results show ongoing restraint amid signs of cost deflation

The first-quarter earnings season has highlighted signs of improved capital spending in the US, while certain tight oil producers have flagged up signs of cost deflation in oilfield services and equipment. Meanwhile, lower gas prices have caused producers in gas-rich basins to scale back operations, while oil prices—which have also declined since 2022—remain strong enough to support activity. Consultancy Wood Mackenzie notes in a report rounding up results among 42 US independents that WTI prices averaged $76/bl in the first quarter of 2023. This is “much closer to a ‘mid-cycle’ level than last year’s average of $96/bl”, it says. “Mid-cycle is not a hard and fast number, but that is generall

Also in this section

28 April 2026

Oil traders warning of $200/bl oil are wrong, and the market should be wary of proclamations that the impact of the oil shortage has only begun to be felt and a that a ‘harsh adjustment’ is coming—even for industrialised nations

28 April 2026

Restoring supply from Saudi Arabia, the UAE, Kuwait, Qatar, Bahrain and Iraq involves complexities far beyond simply adjusting operational controls

28 April 2026

Datacentres will guzzle power at a ferocious rate, but the impact on wider energy markets will be far more complex than previously thought

28 April 2026

The key energy player faces balancing regional routes, political complexities, and creating a clear strategic vision for energy security