There has been no mistaking the industry’s confidence in its future in recent months, not least because of how crisis has pushed energy security, reliability and affordability up the global policy agenda. However, the industry has also accepted the need to tackle the issue of decarbonising LNG, as much as is feasible. The issue of climate change has not gone away.

“The crucial challenge the industry is going to have to address in the coming years is reconciling huge and growing demand for energy, particularly in the developing world, and decarbonisation to prevent the worst impacts of climate change,” said Ed Crooks—former Financial Times energy journalist and vice-chair, Americas for consultancy Wood Mackenzie—during LNG 2023’s final plenary.

“The question of how the LNG industry, as part of the broader energy system, works to resolve those tensions is going to be at the heart of everything we do for years to come.”

Downstream demand

Much of the pull for LNG with low greenhouse gas (GHG) emissions is coming from buyers in Asia because of the demands of their downstream customers.

Its importance will grow as those emerging and developing nations that have made net-zero emissions (NZE) pledges struggle to push coal out of their energy systems, while addressing the intermittency and grid stability issues of renewables such as solar and wind power.

Shell announced at the start of this year that it had just delivered its first “GHG-neutral” cargo—under a verification framework developed by International Group of Liquefied Natural Gas Importers (GIIGNL)—to Taiwan’s CPC. CPC’s Chairman, Shun-Chin Lee, explained: “Demand for addressing GHG emissions from energy use is increasing downstream in Taiwan and we are keen to find new and better ways of meeting this demand.”

He described the pilot cargo as “an important step in improving transparency and accountability of GHG-neutral LNG—not just for us but for the industry as a whole”.

Building trust

These are still early days. While LNG project developers are planning their strategies to reduce emissions across the entire LNG value chain, the imperative right now is to build trust with LNG buyers and end-customers. This makes the measurement, reporting and verification frameworks developed by organisations such as GIIGNL and Singapore’s Pavilion Energy a fundamental first step in the trust-building process.

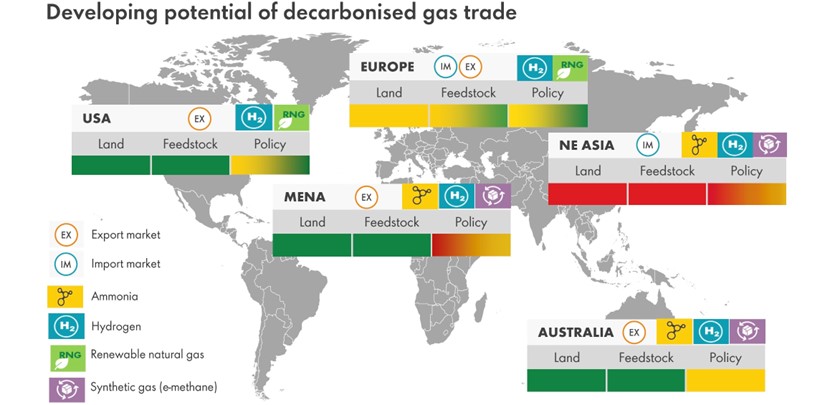

The LNG 2023 conference also provided insights into the longer-term issue of how the vast LNG-importing infrastructure now being constructed in Asia might in future be repurposed for the importation of zero-carbon gases—such as green hydrogen, ammonia, renewable natural gas and e-methane—because it will not be possible to electrify all energy demand.

Analysis conducted by Shell for the LNG Outlook it published earlier this year concluded that North America has “many natural advantages that make the path to decarbonising its gas industry increasingly clear.”

In contrast, Asia—especially North Asia—will find the transition much more challenging. It is likely to have to rely on imports of decarbonised gases to meet much of its demand “in the same way that it relies on imports of LNG today”. In this context, repurposing of LNG import infrastructure would make a lot of sense.

This article is part of our special LNG's role in resolving Asia's trilemma report, which looks at what the energy crisis means for LNG and what LNG's role is in resolving Asia's trilemma. Click here to download the full report, or visit the Gulf Energy Information stand (E326) at Gastech 2023 to pick up a copy.

Comments