The Middle East has made significant investments over the past decade in developing its refining, petrochemicals and natural gas/LNG infrastructure. This move into refined and petrochemical product creation has enabled many countries in the region to diversify their portfolios away from a reliance on crude oil export revenues.

The move to increase petrochemicals production has been aided by the region’s feedstock advantage. Middle Eastern countries have the lowest feedstock costs, providing producers with bigger production margins. The region is also near large demand centres in Asia, which provides an outlet for surplus capacity.

The Middle East is expected to increase petrochemicals production capacity even further through the rest of the decade due to burgeoning industrialisation and urbanisation. This growth will lead to an increase in demand for products produced with petrochemicals.

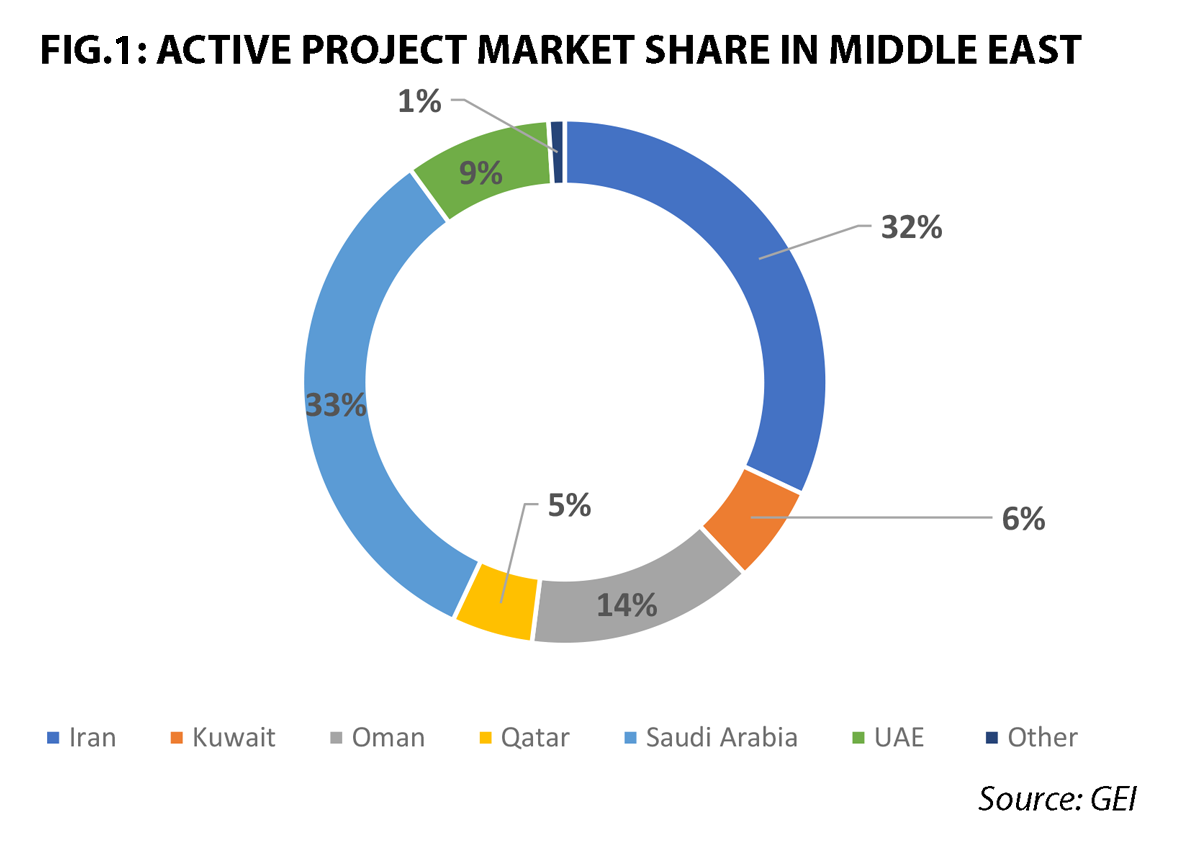

At the time of publication, the GEI database was tracking more than $100b in petrochemical project investments in the region. Most projects are led by Saudi Arabia (33%) and Iran (32%). A breakdown of active petrochemical project market share in the Middle East is shown in Fig.1.

Iran

According to Iran’s seventh national development plan, the country will invest approximately $35b to increase domestic petrochemicals capacity. However, Iran’s goal is to increase domestic petrochemicals production capacity to nearly 190mt/yr in the next 12 years, which will require a vast amount of additional capital. Iran plans to launch more than 100 small and large petrochemical projects at a total investment cost of around $70b; the government has announced the launch of ten new petrochemical unit startups in 2023 alone. If it can build additional production capacity, the country could see petrochemical revenues increase to $180b/yr. Some of the notable projects include:

- The nearly $1.5b, 1mt/yr Gachsaran petrochemicals complex in southern Iran.

- More than $3b in petrochemical projects in the country’s Ilam province.

- The more than $600m Golestan petrochemicals plant.

- The nearly $14b Mokran petrochemicals complex in Chabahar.

- Kangan Petro Refining’s petrochemical complex in Bushehr province.

- PGPIC’s $4.5b Hormoz project.

- The multibillion-dollar Almas Mahshahr petrochemical complex.

- The Kian olefins plant project.

- Petro Tejarat Shahin’s $7.7b Shahid Soleymani Petro-Refinery complex.

Saudi Arabia

Over the last decade, Saudi Aramco has increased domestic refining capacity by more than 1.2m b/d with the construction of the multibillion-dollar JAZAN, SATORP and YASREF refineries. Now, the country plans to focus on developing its petrochemicals production capacity. Saudi Arabia plans to shift about half of its domestic oil consumption from producing transportation fuels to petrochemicals. The country’s energy minister announced in late 2022 that petrochemicals production will increase from 15% of domestic oil consumption to 40%.

To reach this goal, Saudi Arabia is investing more than $15b to build out additional petrochemicals production capacity in the cities of Jizan, Jubail, Ras Al-Khair and Yanbu. This initiative is led by Saudi Aramco and TotalEnergies’ $11b, 1.65mt/yr Amiral petrochemicals complex, which will be integrated into the JV’s existing SATORP refinery, along with Aramco and SABIC’s 400,000b/d crude-to-chemicals complex in Ras Al-Khair—the cost of which was estimated at $20b when it was first announced in the late 2010s. Other notable projects include:

- Alujain’s 600,000t/yr propane dehydrogenation/polypropylene plant in Yanbu.

- Advanced Polyolefins Industry’s more than $1.6b investment to build three plants in Jubail to produce propylene, polypropylene and isopropanol.

- Saudi Aramco and Chinese NOC Sinopec’s new petrochemical complex in Yanbu, for which they conducting a feasibility study.

- Dow Chemical and the Al-Hejailan Group’s MDEA plant in Jubail.

Other Middle Eastern investments. Other Middle Eastern countries are investing in new petrochemicals production capacity to diversify their economies. Some of the notable projects/initiatives are detailed in Fig.2.

FIG.2: NOTABLE PETROCHEMICAL PROJECTS/INITIATIVES IN THE MIDDLE EAST

Africa

The GEI database was tracking more than $70b in active petrochemicals projects in Africa at the time of publication. Most of the region’s investments are in Algeria, Egypt and Nigeria. Combined, these three countries account for 90% of active projects in the region, with Egypt alone accounting for more than 60%.

As part of its Vision 2030 strategy, Egypt is putting money into developing its domestic processing capabilities, including sizeable investments in the refining and petrochemicals sectors. The additional production capacity will help satisfy the increasing demand for plastics, with any surplus destined for export. The nation has already invested more than $5b over the past several years, doubling domestic petrochemicals production capacity to more than 4.3mt/yr. Egypt plans to invest more than $30b in additional petrochemicals production capacity by 2030, as well as spend nearly $20b to significantly increase domestic green ammonia/methanol production. The country’s notable petrochemicals projects include:

- The $11.7b, 3.5mt/yr Red Sea National Petrochemicals complex.

- The $11b, 1.5mt/yr Tahrir Petrochemicals complex.

- Alamein Co.’s nearly $7b, 2mt/yr petrochemicals complex.

- Egyptian Bioethanol’s $112m, 100,000t/yr bioethanol plant.

- ECHEM’s $500m soda ash plant.

- KIMA’s c.$300m, 800t/d ammonium nitrate plant.

- Anchorage Investments’ $2.5b, 1.75mt/yr Anchor Benitoite petrochemicals complex.

- The Suez Canal Economic Zone’s $2.6b methanol and ammonia complex.

- Nearly $20b in green methanol and ammonia projects by companies such as Alfanar, Alcazar, Mediterranean Energy Partners, Misr Green Ammonia, Amea Power, Fertiglobe, Scatec, ANRPC, Green Plant and H2 Industries.

Algeria and Nigeria are also both investing in additional petrochemicals capacity. These investments will help them satisfy domestic demand for plastics. Algeria has several investments to help satisfy domestic petrochemicals demand, including the $1.5b STEP Polymers petrochemical complex, and state-owned Sonatrach’s mixed-feed cracker and butene/polybutene plant, as well as the restart of an ethylene plant in Ras Lanuf that has been on hiatus for a decade.

In Nigeria, Dangote Industries commissioned its 650,000b/d refining and petrochemical integrated complex in mid-2023. Several of Nigeria’s petrochemicals projects focus on increasing production of fertilisers for domestic consumption. Notable projects include Brass Fertilizer’s $3.5b methanol plant, the 2,500t/d Kolmani fertiliser plant, BUA’s polypropylene facility and OCP’s $1.5b fertiliser plant.

This article is from a petchems report which will look in more detail at Asia, the Middle East & Africa, and Europe & the Americas. To read the overview of the report, click here.

Comments